No country for old peakers: price setting in the age of batteries

%E2%80%AF.png)

The dynamics which dictate how the price of electricity is set in Australia have been transformed in the last year, not by policy, but by the unusual characteristics of batteries. Unlike any generator before it, batteries are capable of playing both sides of the price setting equation: supply and demand. Newly compiled data reveals the extent to which the Australian National Electricity Market’s (NEM) price setting agenda has been utterly reconfigured.

As a brief overview, price setting in the NEM reveals a certain hierarchy of least-cost supply, also known as the ‘merit-order’. Dependable coal offers a (relatively) stable price floor; renewables push that floor down when available; while fast, flexible, and expensive gas (and hydro) usually set the price ceiling. Historically, the ‘last unit’ of supply, also known as the ‘marginal unit’, has set the price.

Batteries blur that logic.

If the old world was a one-way street, batteries have created a roundabout, where they can circle between supplying and consuming, influencing the flow and price of electricity from multiple angles.

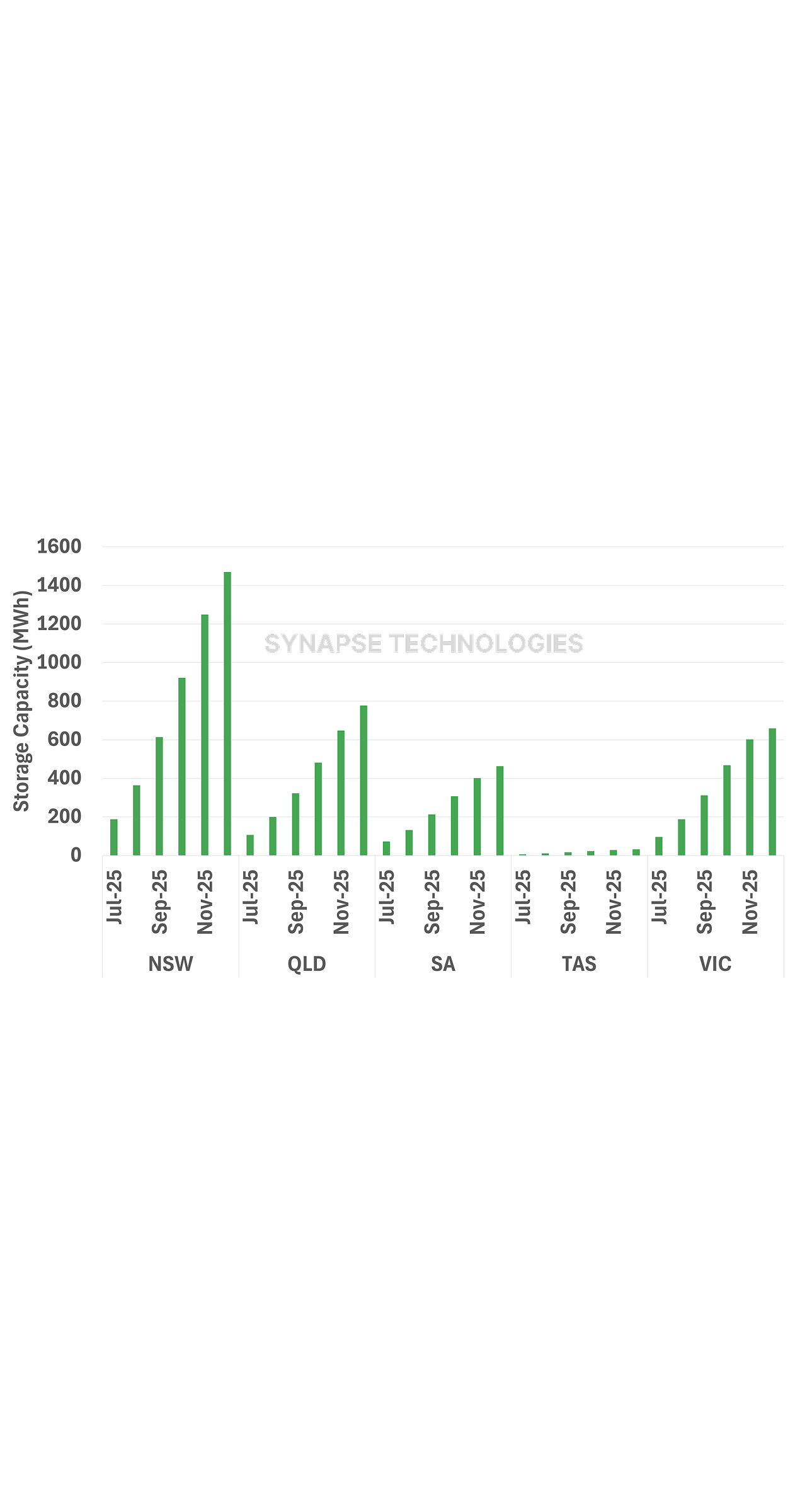

Australia’s battery capacity has scaled from roughly ~0.3 GW in 2020 to ~7.8 GW by early 2026 in all mainland states, and that growth has brought influence. The share of intervals in which batteries set the price has climbed from ~1% in 2020 to ~22% in 2025, with quarterly average for Q1 2026 hitting ~41% in some regions.

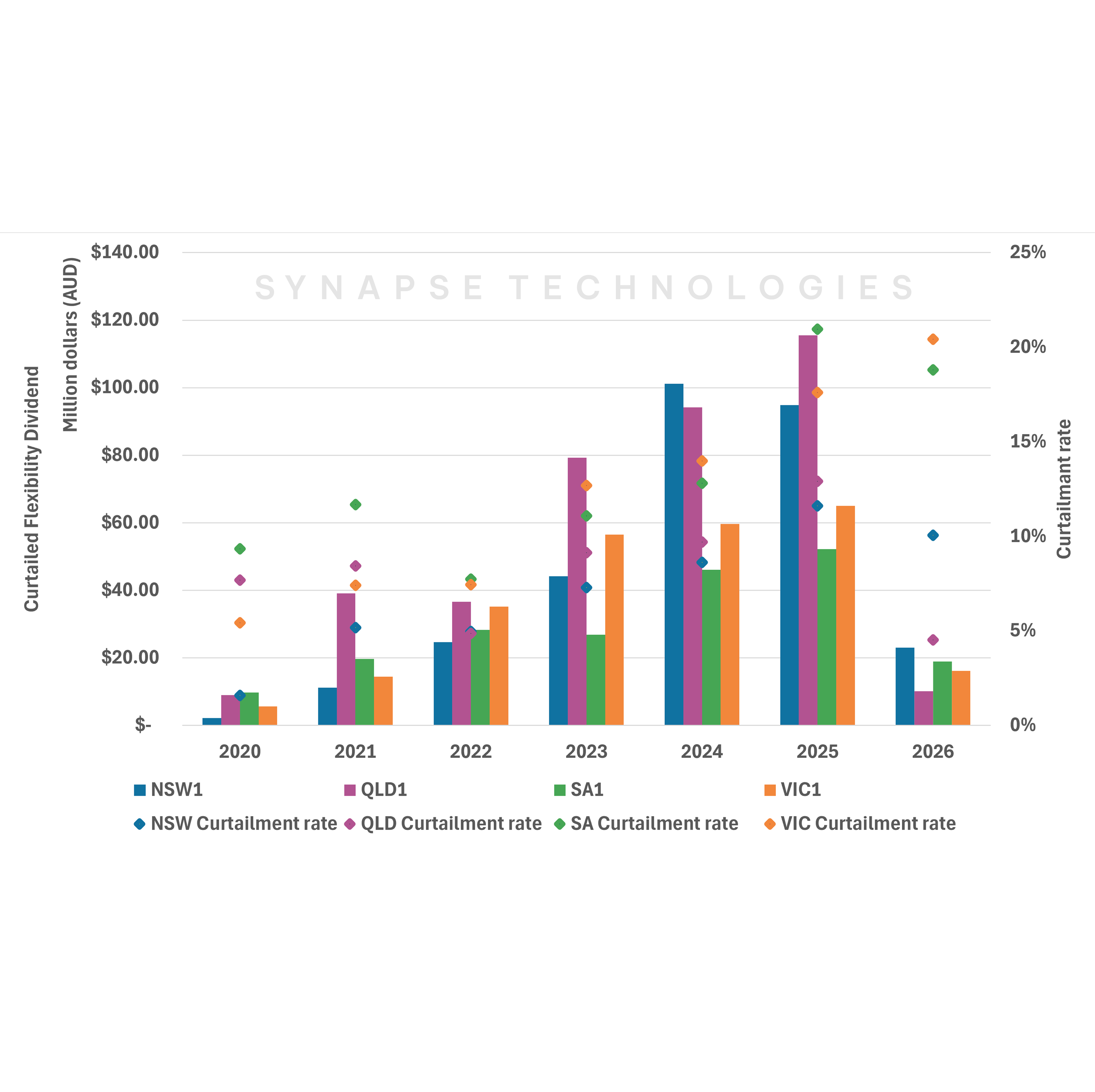

This transformation is perhaps most marked in Queensland, which has gone from effectively zero battery capacity in 2020 to around ~2.6 GW today, with committed projects likely to push that significantly higher. Looking at time-of-day price setting in the state reveals an under-appreciated pattern: the extent to which batteries are replacing gas as the evening price setter. In the evening peak (5 – 8PM), Queensland’s battery price-setting share climbed to ~55%. Meanwhile, in the last 6 years, gas has gone from setting the price in the evening peak about a quarter of the time (23%), to just 5%. Gas is clearly no longer the ‘peaking’ plant it once was.

But that is only half the story.

%E2%80%AF%20.png)

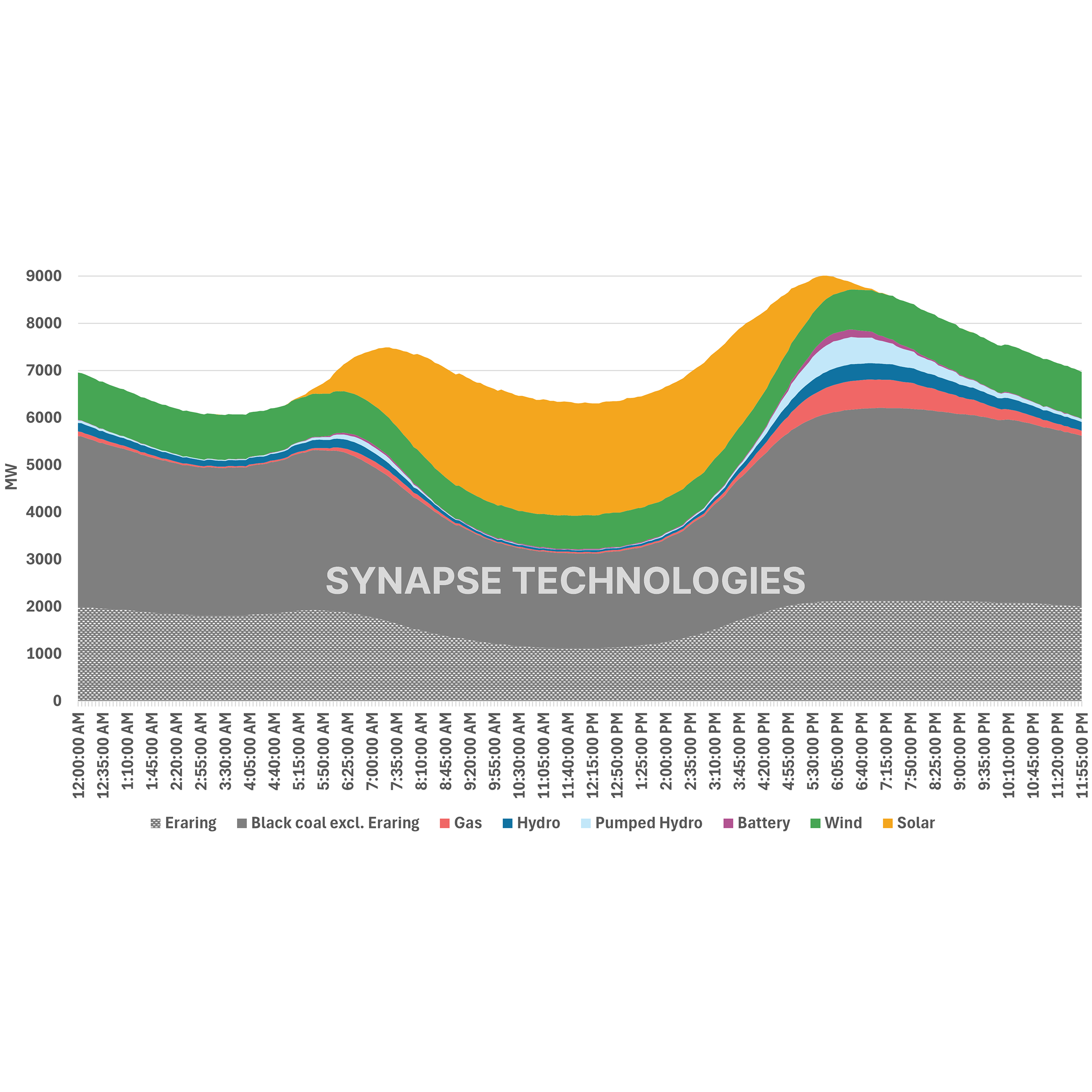

The other half plays out during the day when batteries are in load mode. Batteries’ capacity to charge through the middle of the day is doing more than just soaking up excess solar – it is starting to lift the price floor itself. In Q1 2026, a period typically characterised by strong solar output and suppressed midday prices, average prices between 9AM – 1PM doubled and quadrupled to ~$26/MWh from their Q1 2025 ($13/MWh) and 2025 yearly ($7/MWh) averages respectively. During that same time period, batteries set the price a staggering ~61% of the time, effectively determining the floor of the market during high solar output.

This dampens volatility. Which impacts gas and, ironically, batteries. The difference is that batteries can compete on both ends of the market, while gas is still on the one-way street (supply lane) and expensive. In that context, the role of gas begins to look less like a system cornerstone and more like an opportunistic participant. During extended periods of low renewable output (especially in winter), gas’ role may hold, but such conditions are becoming rarer.

It seems the NEM is entering a new level of maturity, where it has proven that it can return to calmer baselines after periods of chaos that inevitably come with the energy transition. The NEM was designed to respond to price signals. Volatile pricing over the past few years have indeed sent a clear message to the market: the flexibility afforded by batteries is valuable. Investors have responded accordingly, deploying increasingly large volumes of storage.

From that perspective, the rise of batteries in price setting is not an anomaly. It is a direct consequence of the market working as intended. High prices have done what they were supposed to do – attract new capacity. That new capacity is now reshaping the conditions that produced those prices in the first place.

The question is what comes next.

In states like Queensland and New South Wales, this dynamic is likely to amplify. Retirements will create gaps, but those gaps will not exist in a vacuum. They will be met by a combination of new renewables, new storage, and whatever firming capacity remains viable under the evolving price regime. Whether that ultimately creates more opportunity for batteries or preserves a role for gas is still an open question – one we will explore in an upcoming edition presenting future findings from our NEM model developed in Amplink.

.png)