Mind the gap: Data suggests supply holes in NSW’s energy transition

.png)

Questions around supply shortfalls and reliability have reignited in the media this week, budding from forecast consequences of retiring Australia’s largest coal plant, Eraring. Our analysis of current New South Wales data suggests supply gaps do indeed appear likely, namely in non-daylight hours and during the evening peak.

In this edition of Watt’s the Story, we look at the supply gap issue by diving into the New South Wales (NSW) generation mix, quantifying the gap between thermal generation scheduled to retire before 2040 and the pace of wind, solar and storage growth over the past nine years. We break down the region’s grid-scale trends and what they suggest about how quickly NSW’s supply mix is – or isn’t – shifting.

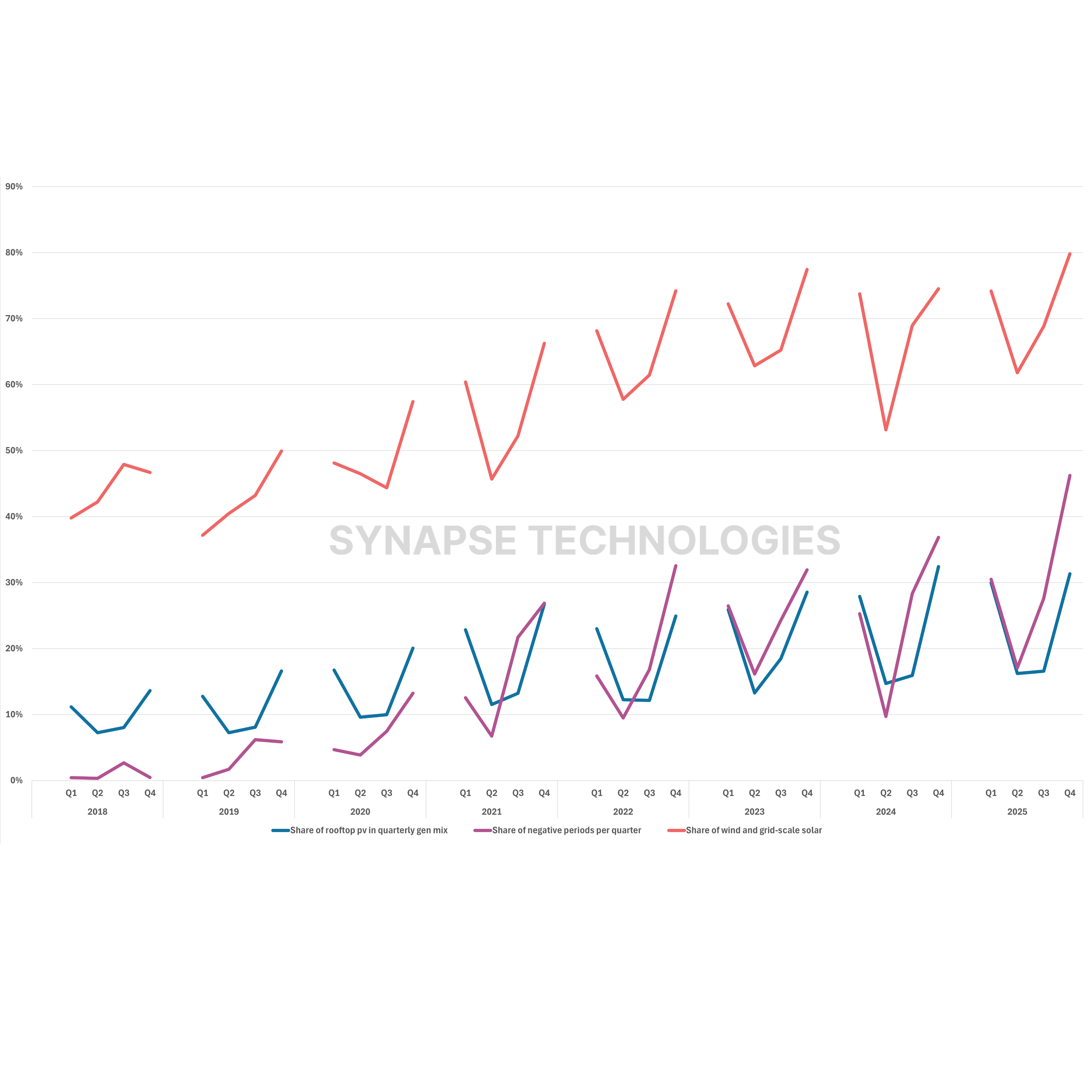

As shown in Figure 1, NSW’s quarterly generation mix has indeed changed meaningfully over the last decade. Since 2017, coal’s contribution to total generation has declined from ~89% to 68%, while renewables (wind and utility solar combined) have risen from 3% (2017 average) to 26% (2025 average) with last quarter (Q4 2025) seeing the largest ever contribution from wind and solar (33%). This shift is material, but it’s not yet a replacement story. Coal remains NSW’s single largest electricity source – more than all other (grid-scale) sources combined.

Even with Eraring’s closure date extended from 2025 to 2029, it remains the case that roughly a quarter (24%) of NSW’s current generation mix is scheduled to withdraw in the next five years. Within ten years, the combined exit of Eraring, Vales Point and Bayswater coal plants removes over half (57%) of NSW’s existing supply. By 2040, with the expected retirement of Mount Piper, this figure jumps to 68%.

From an investment standpoint, this coal retirement schedule represents one of the strongest structural tailwinds in the Australian energy market, signalling long-term investment opportunities due to system level shift. While wind and solar already represent consequential new electricity sources, Australia’s hyped utility-scale batteries remain an extremely small contributor at just 1% of the current supply mix, underscoring just how early Australia’s firming build-out still is. Moreover, it suggests that fears about battery ‘saturation points’ and diminishing arbitrage opportunities are likely unwarranted.

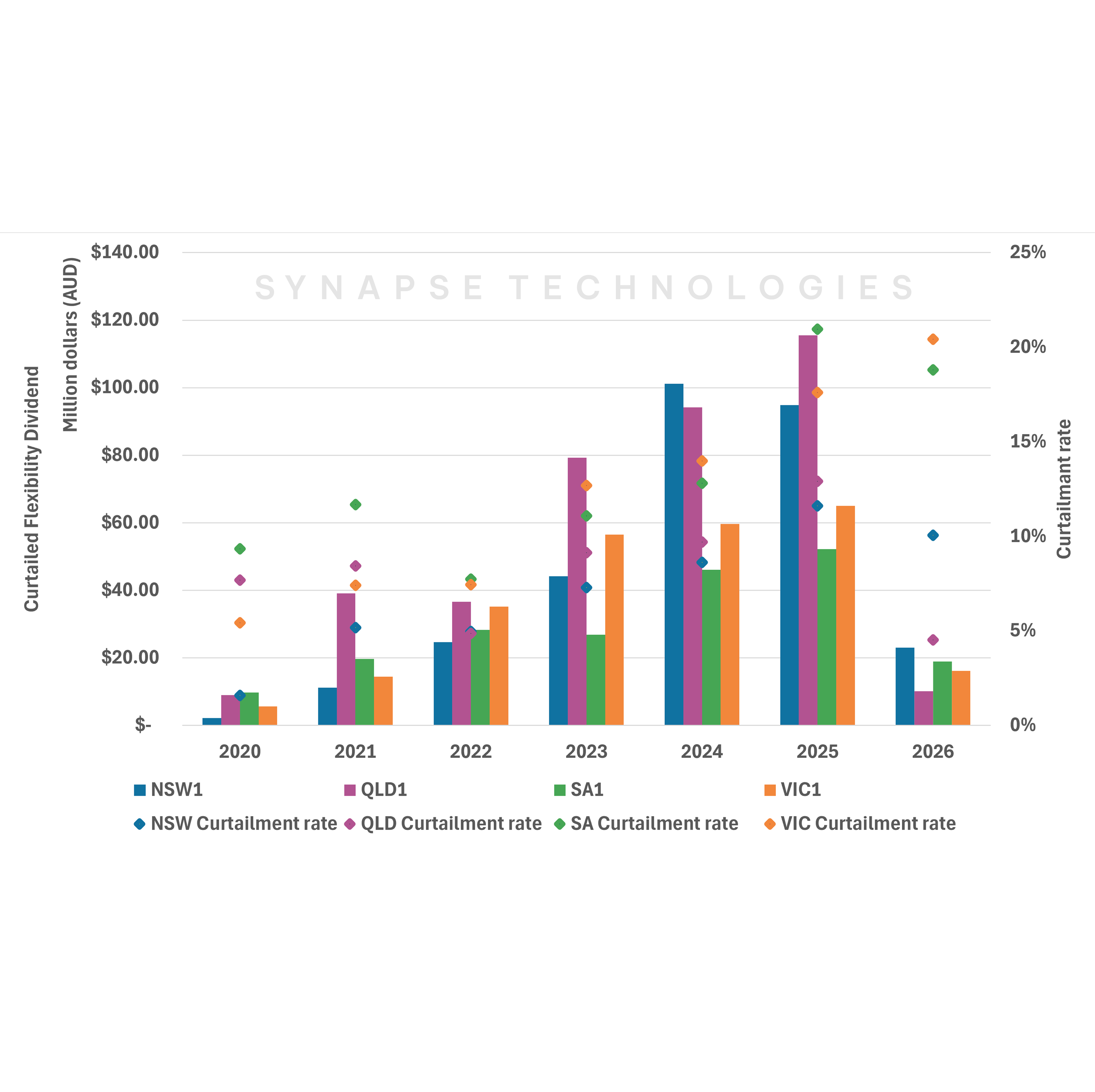

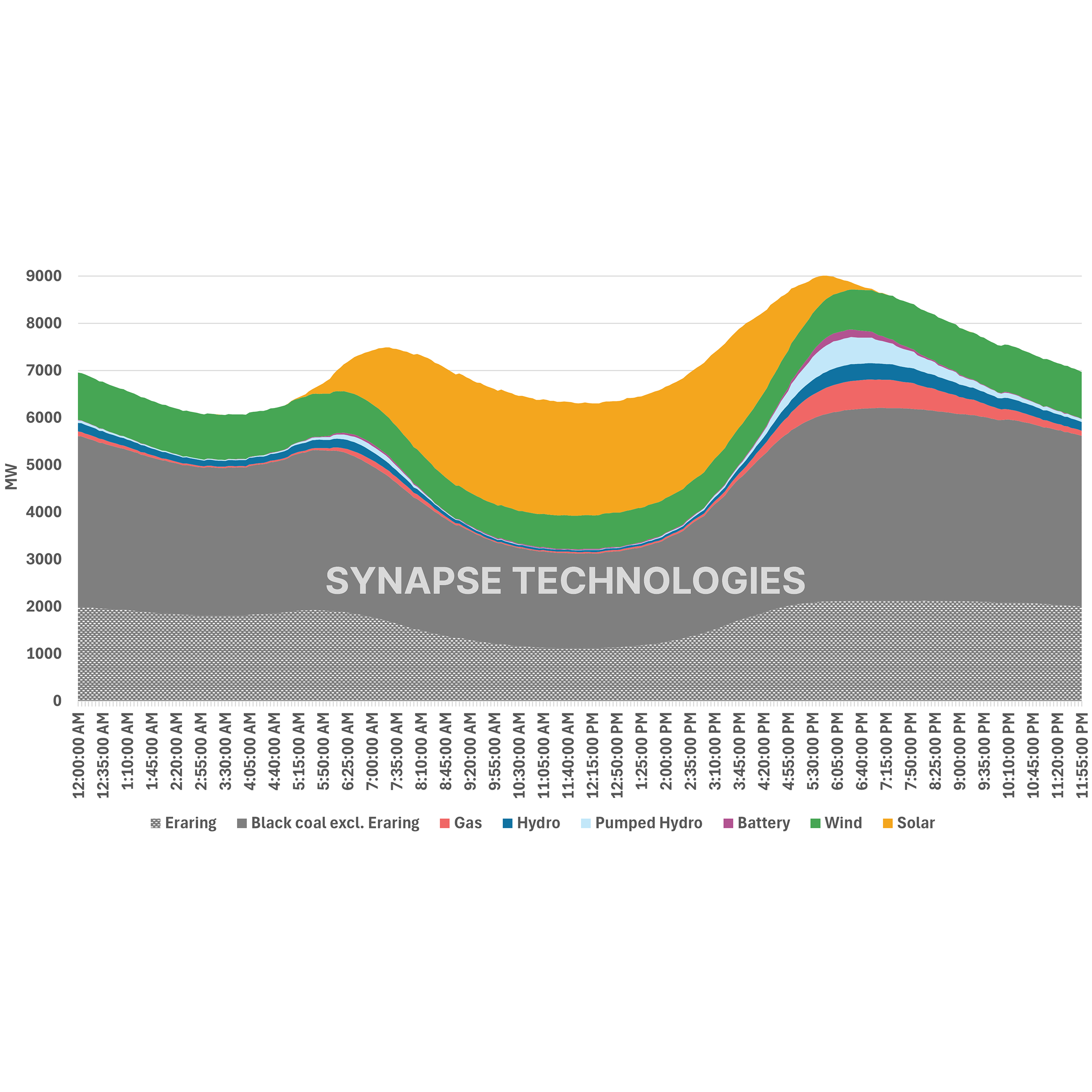

In fact, as seen in Figure 1, had Eraring exited in August 2025 as initially expected, NSW would have had to replace a power station contributing almost as much energy as wind and solar combined over the last year (24% vs 26%), more than both in Q2 (28% vs 20%), and matching them in Q3 (23%). Given its ‘baseload’ profile, Eraring’s output is disproportionately valuable in the evening peak (when solar generation - both grid-scale and rooftop - tapers off, exposing higher net load) especially on low wind days. This point becomes particularly apparent when we take a closer look at the NSW generation mix on a time-of-day basis.

.png)

As seen in Figure 2, in 2025, Eraring alone supplied approximately 30% (80% for all coal generators) of the state’s energy outside solar hours (7PM – 5AM), compared to 18% (50% for all coal generators) during the day (9AM – 3PM). This trend suggests that its exit would have almost certainly led to a spike in intraday volatility and a strong bull market for NSW batteries in 2026. Figure 2 also shows that batteries in NSW have room for substantial growth given all remaining coal generators are scheduled to retire by 2040, especially so since their operational profile aligns with the system need for intraday flexibility. In addition to the intraday volatility driven by solar, seasonal volatility trends are also emerging due to irradiation variance. As seen in Figure 1, renewable generation share in winter (Q2) is consistently the lowest across quarters and this seasonal difference is growing. Consequently, coal generators are increasingly having to do more in Q2 compared to other quarters (71% in Q2 vs 61% in Q4, 2025).

It remains to be seen if prolonging the operations of aging coal plants actually translates into dependable supply, particularly as the grid’s seasonal and intraday profile becomes more volatile and thus requires harder ramping from coal generators. The impending supply gap from coal exits remains steep, with the market urgently needing storage assets to grow alongside renewable capacity. As it stands, NSW’s energy transition remains on track in direction, but not yet in speed. As we continue to develop our long-term NEM models in Amplink, we’ll be further analysing the complexities of the energy transition.

.png)